Money makes the world go ‘round.

While you may have tamed the fantastic plastic in your wallet at home, it can be a whole other game when you travel overseas. There are exchange rates, bank fees, and ATM surcharges to contend with, not to mention risks like card skimmers and dodgy currency changers.

Should your money go wrong at home, you’ve probably got a fall-back plan or friends and family to help out. On the road the potential for a major disruption is much greater.

As I’ve travelled around the world, I’ve learned a lot of lessons about how to make my money last longer, and keep it safe. Some the easy way, and some the hard way. And now I’ve put them together into this beefy melt-in-your-mouth article that will set you in the right direction towards holiday happiness.

As a prefix, these 72 tips and strategies are universal regardless of your home country, preferred bank or financial institution, and are relevant worldwide. Also, I’ve deliberately left out the topic of credit card points. That’s a completely different beast and best practices vary broadly between countries. Today I’ve purely focused on keeping your hard-earned dollars where they belong… in your pocket.

To make them easier to digest, I’ve divided these juicy morsels into 6 categories: debit cards & credit cards, prepaid travel cards, ATMs, currency exchange, security, and planning & strategy.

Let’s dive in!

Debit Cards & Credit Cards

Money comes from somewhere. And while I wish it would be trees, chances are your money is currently sitting in a bank account somewhere in the world. If you’ve got wads of cash stuffed in your mattress, then all I can say is that I hope you sleep soundly at night. Choosing the best mix of debit or credit card for travel will depend on your specific circumstances, spending patterns, and comfort with risk but these guidelines will cover most bases.

1. Do your homework. Don’t wait until you’re 10,000 feet in the air to think about managing your travel money.When you’re at home,find out which card will offer you the best features and benefits, with lowest (or zero) fees. It’s too easy to just pull out your existing debit/credit card and cross your fingers. But don’t do it. If your research shows that your current cards are the best choice, then great! Better to be safe than sorry.

I currently use Xinja as my go-to card. It's independent & Australian with zero fees - it charges no ATM fees internationally, refunds 100% of currency conversion fees, and has no other fees at all. The mobile app is super simple and lets you lock your card if you're worried about security. Plus, its shows the exchange rate you paid, and the amount in AUD and the local currency. Couldn't ask for more!

Xinja tip: if you are asked to choose an account type during a point-of-sale transaction or an ATM or , opt for "credit". This will ensure your skip the fees.

Popular country-specific card research websites are: Mozo and Finder (Australia), Creditcards.com (US), Ratehub (Canada), Moneysupermarket.com (UK). What card features should you specifically look for in a card? Glad you asked!

2. Transaction fees. Avoid foreign transaction fees like the plague. These can be charged separately or sneakily rolled into the total transaction amount, and can be up to 3.5% or higher. You can always find this figure in the debit/credit card fine print. Here’s a scenario: on your 10-day vacation if you spend $2000 on a hotel (usually billed on-site), $1000 on eating out, $1000 on shopping and gifts, and $750 on attractions then a 3.5% foreign transaction fee would add up to $166.25! Yikes! That’s a lot of mojitos.

3. Cash advance fees. These fees apply to credit cards when withdrawing cash from an ATM. Only stoop this low if it’s your last resort. It’s not a mortal sin - just pay it off as soon as you get back to your hotel/apartment otherwise you’ll be paying interest on that straight away rather than enjoying the usual benefit of an interest-free period. Depending on your bank, they might be cheeky and start charging interest on your entire balance – not just the amount withdrawn. Fine print, people!

4. Monthly & annual fees. I try to avoid monthly and annual account keeping fees wherever possible. The only case this should be allowable is for a credit card that offers super-duper awesome rewards and you make your annual fee back at least 3 times over. So, if the annual fee is $100, you should expect a minimum of $300 in value (either rewards or bonuses). For a debit card, your bank may charge a monthly fee if your balance is below a particular threshold. I’d try to avoid these cards but if you can’t, always stay above that figure to avoid the fee.

5. Choose chip cards. These use an EMV chip instead of a magnetic strip to store your sensitive data, offering better security and making it harder for scammers to skim. These types of cards are now standard issue in Australia, Europe and Asia, but only recently rolling out in the United States. If the mag strip is still present then the card will be backward compatible with older terminals but present at a higher risk to skimming (see more details below about security).

6. Check your card expiry date before leaving. If you get stuck with an expired debit or credit card while overseas, it can be a pain to get your replacement card sent to an alternative address. If you need to arrange a card renewal before departure, many financial institutions can manually initiate a renewal up to 90 days early if you simply ask.

7. Avoid cancellation for non-use. Some financial institutions either charge a fee when the card is not used for a long period of time or cancel it altogether. The audacity! Test your cards before departure in case any infrequently used cards have been deactivated by your bank.

8. Ditch the cards. Avoid pulling your card out altogether, and use your phone instead. Welcome to the future, my friend. All you need is a supported NFC-enabled phone (which includes most modern smartphones) and supported bank account. The 3 most popular digital wallets are: Apple Pay, Google Pay, Samsung Pay. These work by generating a temporary transaction token on the fly each time you pay so even if the data is somehow skimmed then the token cannot be reused and your primary card is not jeopardised. Keep in mind these digital wallets are not supported in every country or every bank yet (check support for: Apple Pay, Google Pay, Samsung Pay).

9. Use internet banking. If you’re not doing so already, set it up today. You’ll need it. I’ve heard of travellers being stuck overseas with no way to add funds to their card because they never used internet banking before. Please don’t be like that. If my tech-unsavvy mother can get on board then you don’t have an excuse.

Prepaid Travel Cards

These types of cards have grown in popularity over the last decade. As international travel has boomed, savvy spenders have moved their spending money to separate cards to reduce the fraud exposure of their primary day-to-day bank accounts. But be careful because not all prepaid travel cards live up to their promises. Read the fine print to understand what the real fees are. For Australians, Xinja's prepaid card is a perfect example of what a travel card should be. Comparisons of popular travel cards can be found on: Canstar (Australia), Cardrates.com (US), GreedyRates (Canada), Moneysupermarket.com (UK).

If you do not choose carefully young Padawan, then expect a death by a thousand cuts. The tiny fees will eat away at your stash of cash and vex your vacation.

10. Card issue fee. This hefty wallop often gets taken off the card value if you purchase it from an off-the-shelf retailer and can be as high as $10. Ideally you want this to be zero.

11. Prepaid card loading fees. Some financial institutions charge a one-off loading fee (up to $15) the first time you use it. Others charge for each reload.Ideally, you want this to be zero as well, but at the very least a small once-off loading fee.

12. Avoid preload cards that fix the exchange rate. Let’s be frank. It’s never going to work out in your favour. The sales pitch seems compelling - hold multiple currencies (up to 11) and avoid exchange rate surprises. Ohhh, I’m giddy just thinking about wads of virtual currency in my greedy little hands. Don’t be tricked into setting your exchange rate before departure - it’s never the best possible rate. The same rule applies to casinos… the house always wins. The only exception to this rule is if your home currency is subject to hyperinflation like Zimbabwe. Chances are it’s not.

13. Low withdrawal limits. I don’t understand the logic of travel cards that have low ATM withdrawal limits such as $200 per day. You’re on vacation! And those fancy cocktails with the tiny umbrellas at the beach club don’t come free. Check the ATM withdrawal limits beforehand so you don’t get stuck.

14. Reload delay. Just imagine reviewing your travel card balance and realising you’ve got just $50 remaining. No problem! Just transfer more funds from your regular savings/checking account. Unless your card delays reloading up to 3 days. Then things could get awkward very quickly. Check this in the fine print.

15. Account inactivity. Use your card and get hit with fees. Don’t use your card and get hit with fees.For the sake of everything that is sweet and innocent in this world, please don’t get a card that charges you for inactivity. It’s a crime. And if the card charges an account closure fee, just say no. Some cards even charge a fee if you want to refund the balance onto your regular savings/checking account. The audacity!

16. Replacement card costs. What happens if your card gets lost or stolen? Hopefully that never happens but check the fine print for costs and timeframes. These kinds of surprises aren’t fun.

17. Not usable everywhere. While you can use a reloadable Visa or MasterCard wherever the logo is displayed, certain types of merchants won’t accept prepaid cards such as car rental companies, some petrol stations and even toll booths. In addition, some travel cards do not support online purchases. Depending on your spending patterns this may or may not be an issue when travelling. But it pays to know upfront.

18. Non-reloadable. Some prepaid cards are not reloadable which limits their usefulness. So don’t just grab the first prepaid Visa card you see at Walmart and expect a happy vacation. Not going to happen.

ATMs

Cash is king. And in some countries, it’s the most common way to transact. Sure, debit and credit cards offer convenience, but haggling with a street market vendor in Bali or Phuket won’t work so well when you flash out your MasterCard. You can either bring your own cash from home, or withdraw it from an ATM in your destination.

Money tip: There's a lot of short-term offers from financial institutions, check out these best bank promotions to stay up to date.

19. Nasty foreign ATM fees. These are typically up to $5 per withdrawal, but if you’ve done your research they’re possible to avoid. In the US, Charles Schwab Bank offers a checking account with unlimited ATM rebates worldwide. In Australia, Xinja offers free ATM withdrawals worldwide. If you have no other choice, then I suggest getting out as much cash as the ATM will allow as this will reduce the flat ATM fee as a percentage. For example: a $5 ATM fee on a $100 withdrawal is 5% (ouch!), whereas a $5 fee on a $500 withdrawal is just 1% (much better!).

20. Watch out for local ATM owner fees. You might think you’re as cool as David Hasselhoff (in 1982) knowing your card issuer doesn’t charge ATM fees, but watch out. Local ATM owners can charge their own flat fees. Getting hit twice for a withdrawal can really add up. Same rule as the previous point, take out as much as you can, or see a later point about ATM alliances.

21. Keep ATM card balance limited. Divide and conquer. Only keep as much money as you need on your ATM card, and keep the rest in a savings/checking account that is not accessible via your ATM card. As you need more money, just transfer it to your ATM card via internet banking. This way if your card gets stolen or skimmed, the damage can be contained. Even if your bank protects you from unauthorised transactions, it can take weeks to get the funds back.

22. Reasonable ATM cash withdrawal limits. Check your card’s limitations before departure. To limit potential damage if your card is stolen or skimmed, many bank accounts support the ability to set ATM withdrawal limits via internet banking. Use this option at your discretion. A clever idea is to set your withdrawal limit to $0 (or a low number), then before you leave the hotel to find the nearest ATM, increase the limit, then lower it when you get back. Call it over-cautious, but it works.

23. Regional ATM withdrawal limits. In some developing countries, such as Indonesia, the ATM withdrawal limits are low in comparison to your home country. I found the typical ATM limit in Bali, Indonesia is 2 million rupiah (around AU$200 or US$142). When I found one particular ATM that allowed 3 million rupiah, I thought all my Christmases had come at once! In these kinds of situations when you need more cash, doing multiple withdrawals back-to-back makes sense. Just be aware each time you may be attracting a bank fee from your financial institution. In those situations, it’s usually better value to have a wad of cash in your home currency and change it over the counter at a money changer (see later points for tips).

24. What if you get blocked? Call your bank straight away and try to sort out the cause of the block. Chances are their fraud detection system flagged your transaction incorrectly, and they’ll be able to re-activate your account straight away.

25. Basic ATMs. Foreign ATMs usually have a limited range of functionality – you’re pretty much guaranteed to get a machine that will handle a withdrawal. Potentially you can view balances. But for anything more detailed, such as transferring funds between accounts or changing PINs, you’re better doing that via internet banking.

26. Check vs savings. Know your account type before you travel. In the United States, the most common transactional accounts are called “checking” (“chequing” for the more cultured folks in the UK and Australia). Whereas these are called “savings” accounts in Australia. If you try to pull out money from a “checking” account at an ATM and select “savings”, it will probably return a message saying this action cannot be performed. Just run the transaction again and choose the alternative account type.

27. Only use an ATM in a language you understand. It might sound like common sense, but if you’re desperate in a foreign country and cannot understand the commands and options, you might get yourself into a lot of hot water. The majority of ATMs around the world offer an option to use the interface in the local language or English. And since you’re reading this article, I can safely assume you can read English. As a back-up I like to use the Google Translate app which can convert an image taken by your smartphone into your preferred language on the fly.

28. Use reputable ATMs. Pick ATMs belonging to banks where possible rather than those found in hostels, hotels, or convenient stores. The stand-alone independent ATMs often have higher fees and a lower withdrawal limit.

29. Daylight is your friend. Where possible, do cash withdrawals during local business hours. If your card gets eaten by the ATM, then it’s easier to rectify the situation by calling the phone number on the ATM or just walking into the nearest branch.

30. Set a 4-digit PIN. If your home ATM supports a 5-digit PIN then change it to a 4 before departing as some ATMs around the world only support a 4-digit entry. This can typically be done at your home ATM or via internet banking.

31. Memorise your PIN. Don’t write it down on your phone or a piece of paper. If your memory is so bad that you have to write it down, at least encode it so a would-be thief could not decipher it.

32. Shield your PIN. When entering your PIN number into the ATM, use your other hand and/or body to obscure the view of the keypad from a potential “shoulder surfing” thief.

33. Stay alert. Watch out for anyone lurking near an ATM. Often thieves work in pairs, and one will distract you while the other grabs the cash. If you feel uneasy at all, just walk away and find another ATM. It’s not worth the risk.

34. Beware of stuck cards. This is a classic scam for fraudsters to gain your PIN number if you attempt to enter the number again while they’re watching. After you leave, they can eject the card and start using it. It’s best to not leave the ATM, and call the bank to resolve the issue. Or if in doubt, call your card issuer and block/cancel the card.

35. Inspect the machine for a card skimmer/shimmer. Look for anything out of the ordinary such as:

- crooked or loose card slot

- bulging card slot

- card slot with mismatched colour

- glue residue around card slot

- typical flashing lights below the card slot not working

- engraved arrows near the card slot that are too close or overlapping (indicating a skimmer has been attached to the slot)

- thin card inside the card slot (called a “shimmer”)

- small camera mounted nearby pointing at the keypad

- loose keypad

When in doubt, the rule is “wiggle”. ATMs are built to last, so feel free to jiggle any protruding parts like the card slot, push firmly on the keypad. Wiggle your card as you enter it in the slot – this can foil the shimmer inside the machine.

A compromised ATM will likely still perform correctly but the fraudster will return later to collect the harvested data and use it to either break into your bank account or create clones of your card. Also, ATMs are not the only devices that can be compromised, the risk applies to fuel stations pay-at-pump devices and in-store card terminals. If you don’t know what to look for, here’s a useful YouTube video.

Currency Exchange

The vast majority of merchants only accept their own local currency, and that is usually required by law. There are some notable exemptions, particularly in locations like the Caribbean where US Dollars are widely accepted thanks to truckloads of American tourists that descend on beautiful tropical islands daily, but don’t take that for granted all over the world. Converting cash from one currency to another opens a plethora of pitfalls that can whittle away at your vacation kitty.

36. Know your numbers. Get live currency exchange rate ahead of time. I recommend XE.com. Don’t rely on your bank as they may skew the rate in their favour by several percent. To understand the lingo, “interbank rate” is the wholesale rate banks give each other which is typically much better than “bureau de change” rates (currency exchangers on the street). I used to write down standard conversions on a piece of a paper (or phone) so I could quickly reference them when shopping. Now the Xinja mobile app shows transactions in the local currency as well as AUD.

37. Install XE app. Set up the currencies you’ll use on your smartphone. And learn from my experience – do this while you have Wi-Fi access, once you’re out and about it might be too late. I tend to have a handful of key currencies (AUD, USD, CAD, EUR, GBP) along with the local rate. One time I was transiting through Kuwait International Airport and needed a drink which only cost 7 Kuwaiti Dinar. Turns out this cost US$23… ouch!

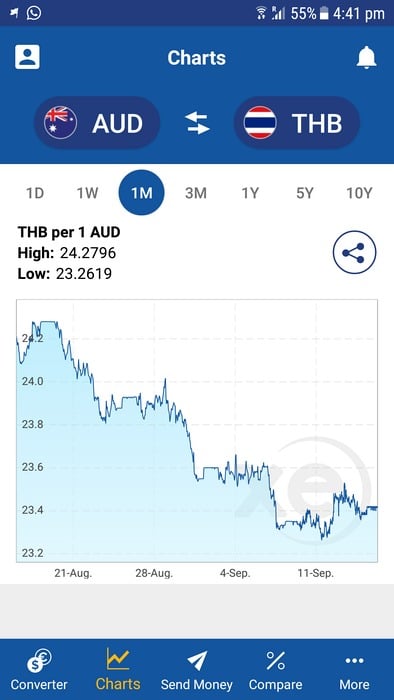

38. Ride the XR wave. If the exchange rate trend appears to be moving in your favour, hold onto your home currency as long as possible and only change what you need. If it’s going south, then change as much as possible quickly and spread the cash so it’s not all stored in one location. Even better, keep the surplus in your hotel safety box. You can find this info on the “charts” button in the XE app. Set the time period to 1 month and you’ll get a good idea of where things are heading. See the screenshot below where I could tell the Australian dollar was losing ground to the Thai baht and it was time to hit the ATM hard.

39. Do it overseas. When changing your home currency to foreign, it’s usually better to do it at your destination rather than in your home country. This is most obvious if your home country has a “strong” currency (such as USD, CAD, AUD, GBP, EUR) and the foreign country has a “weaker” currency.

40. Choose local. At ATMs or in-shop card purchases choose the to pay in the local currency (not your home currency) so your financial institution works out the exchange rate. Chances are the exchange rate offered by the merchant’s bank won’t be wonderful. If you picked a smart card with zero exchange rate fee, this benefit would become worthless.

41. Note all notes are equal. With some major currencies like US dollars and Euros, it’s not uncommon to have one exchange rate for larger notes ($50, $100) and a lower exchange rate for smaller bills ($5, $10, $25). If you’re brining currency from home, it can pay to bring larger notes. And don’t expect that obscure currencies will be easy to change overseas. I tried changing some annoying Serbian Dinar in Indonesia and no money changers would touch it.

42. Be careful where you exchange your cash. Look for a reputable registered money exchanger. They should not charge a flat commission and the rates should be publicly displayed (even a hand-written piece of paper taped to the booth window is fine). The benchmark for trust will vary from country to country. For example, in Indonesia or Thailand I would use an exchanger if they had a permanent location, usually air conditioned. Staff should wear a uniform or smart attire. A wooden booth on the side of the road manned by a guy in a grubby singlet would be best avoided.

43. Get it in writing. Obtain a receipt before agreeing to the transaction. In some countries this is legally required. I use the calculator app on my phone to double check the final figure is correct.

44. Check it twice. Double check the cash you’re given before leaving the counter. Once you leave it’s too late. Don’t feel pressured if you’re holding up the queue.

45. Carefully inspect currency for potential counterfeits. Depending on the currency, look for a watermark or translucent panels. If you’re not happy with any notes, ask the clerk to replace them.

46. If the exchange rate is too good to be true, it probably is. This is a tell-tale sign of a scammer. I tried an exchanger in Bali and when he tried to short-change me, I called him out and forced him to hand over the correct amount. When I realised my win, I asked to exchange another $50, and he said he was out of money and closed down for the day… very conveniently. If you’re not happy with the service or are concerned about a scammer, take a photo of the money changer and note down the address (or drop a pin in your Google Maps app) then notify the nearest tourist police branch.

47. Don’t change money at the airports. These often have the worst rates. Travelex seems to be everywhere I’ve been but usually have the worst exchange rates. Converting at a bank branch is a last resort. In much of Asia I find exchangers on the street have very good rates due to the relatively low cost of labour.

48. Departure tax. If you need cash to pay for a separate departure tax (depending on the country), remember to hold onto the exact amount in your wallet. Once you get past the immigration desk, there’s less chances of finding a currency exchanger or ATM. I got stuck once at an airport immigration desk with insufficient cash and had to walk back to the entrance of the airport to find an ATM. Most sensible countries now bundle the fee into the airline ticket prices.

49. Get rid of coins before you leave. These often cannot be changed by exchange bureaus, so try to use them up before flying back to your home country. On occasion I’ve give those little round metal things away to those in need, and it helped to brighten someone else’s day.

Background image created by Freepik

Security

No doubt you’ve heard stories of travellers being the victims of theft or fraud, but in reality, travel is safe in most countries by following a little common sense. Here’s how you can safeguard your cash and cards while travelling.

50. Notify your bank. Most banks allow you to notify them of travel plans via their internet banking system. This helps their fraud detection team know where you intend to be in case a transaction comes up where you haven’t been before.

51. Spread your money. Store cash and cards in several separate locations such as a wallet, purse, backpack, in your socks, etc. This way if one bag gets stolen or lost, you haven’t lost all your cash/cards.

52. Consider a money belt (aka bum bag/fanny pack). I’m far from the world’s most stylish traveller (most days I don’t even brush my hair), but I just can’t bring myself to wear a money belt. Nevertheless, I can’t deny that they work. For a more discrete option, wearable travel pouches placed beneath clothing is a good idea if you’re concerned about your cash.

53. Push it. If your financial institution supports it, enable mobile push notifications for every transaction on your card. This way there’ll be no nasty surprises if your card is stolen or skimmed. I recently received several notifications for my credit card when I knew it wasn’t being used. Within seconds I called the bank and disabled the card.

54. Check your bank transactions daily. If your card provider doesn’t support mobile push notifications, check your transactions at the end of each day. If something looks suspicious then report it to your bank straight away.

55. 1-click card locking/freezing. If your mobile banking app supports locking or freezing of your card, then get familiar with this functionality before departure. This way if the card gets lost or stolen you can deactivate it temporarily. I love this feature in the Xinja mobile app.

56. Keep ‘em separated. Load travel funds onto a separate card from your regular “at home” spending. This way if the card is compromised then you don’t have to waste your time setting up all your direct debits again.

57. No touchy touchy. Even better, use contactless payments wherever possible. This reduces the chances of your card being skimmed by a compromised ATM or retail terminal.

58. Avoid doing internet banking on open public Wi-Fi networks. Public Wi-Fi networks that do not have a network password (often found in cafes and airports) have a greater risk for digital eavesdropping. If you can’t avoid these, I recommend using VPN software (such as Norton or ExpressVPN). Or even better, use a personal Tep Wireless hotspot while travelling (like me!).

59. Avoid pulling out your wallet in a busy location. It will be more susceptible to a snatching, particularly if you’re flashing lots of currency around. Find a quiet spot and stay aware of your surroundings.

60. If your card is stolen act quickly. Call your financial institution to put a hold on the card and report unauthorised transactions. The maximum liability you could be forced to carry is $50, but in most cases, it will be zero.

61. Don’t let your card leave your sight. If you’re at a restaurant, it is preferable for the waiter/waitress to bring a mobile card terminal to the table or for you to stand up and walk to the cash register. A well-known scam perpetrated by waiters is to skim the card through a concealed duplication machine. This data is then sold to scammers who duplicate the card or attempt to break into the bank account.

62. Keep a written list of important phone numbers. Should the unfortunate happen, you will have all the information at your fingertips: credit card issuer, family/friends, travel insurance, embassy, and local police. It’s also a good idea to write down an encoded form of your account number so if your card gets stolen you can easily identify yourself when calling your bank.

Planning & Strategy

You know the old axiom about “an ounce of preparation”. Planning ahead when it comes to spending money overseas can save your bacon. And while we hope for the best, it’s prudent to prepare for the worst. This way what might have been a total disaster only becomes a minor inconvenience.

63. Carry a back-up card. Or two. Don’t take more cards that you need to, but having a fall-back plan should one of your cards be compromised or blocked by your bank will add to your peace of mind. If your two (or more) cards are from different banks, then you’ll be safe in case of a bank-issued block or cancellation.

64. Have at least 1 Visa or MasterCard. Amex and Diner’s Club are not widely accepted around the world regardless of what their advertising jingles say. And in some countries if these less common cards are accepted, a percentage-based transaction fee may be levied by the merchant.

65. Check your bank card’s ATM alliance. In some situations, ATMs from foreign financial institutions aligned with your home bank provide discounted or free withdrawals. Check the fine print of your debit/credit card for details.

66. Know where your nearest ATMs are. I prefer to use Google Maps (just search for “ATMs” or click here) but it’s not foolproof. Visa and Mastercard also offer online ATM locator services.

67. Look for the card network logo on the ATM machine. Visa owns the Plus network, and MasterCard owns the Cirrus network. While these two types of cards will cover you in most countries, do your research ahead of time. In Japan you’ll be hard-pressed to find ATMs that accept international cards (tip: most 7Elevens or post offices have ATMs that will work). And strangely enough many Japanese ATMs are switched off at night (after 7pm weekdays, 5pm on weekends). To give you a heads-up before you travel, here’s a list of countries with the most numbers of ATMs per capita.

68. Bring at least US$50 cash with you just in case. You never know when you’ll need it. Either for taxi or an impromptu hotel/hostel room or a tank of petrol. If you have more than you need for 1 day’s travel, leave the rest locked in your hotel room’s safe.

69. Vacation loans. While I usually recommend saving for travel, if you're in a situation where you need to borrow money, consider a vacation loan. This typically attracts a lower interest rate than credit cards and personal loans. Do your research online to find the best vacation loan options.

70. Act like a local. If you’re thinking of staying in a new country for more than 3 months, it might just be easier to get a local bank account. In most countries, it’s relatively easy to get a checking/savings account (credit cards are another issue). Wiring or transferring your funds in bulk from your home country to the new country probably will work out cheaper for large sums (over $10,000).

71. If you’re thinking of using traveller’s cheques, I’ll just say one thing. Don’t. This is not 1985. There are virtually no security benefits and very few merchants accept them anymore. I’ll divert your attention to point #9, use internet banking.

72. Have fun! What’s the point of having money if you don’t enjoy it. Don’t get too uptight about travelling, just tighten the seatbelt and enjoy the ride. Once you’ve done everything you can - completed your homework, made all the necessary preparations, and setup fall-back plans - then it’s time to enjoy your hard-earned vacation and go where the road leads.

Reader Comments...

"I respond to every comment by direct private email. I look forward to your feedback" - Josh Benderhave a small list what I’m doing before every travel. Firstly I separate my travel money, I never have all my money in one place. After I exchange some local currency, also I take more attention for my privacy, so I always have with my self nordvpn for my data protection, and finally, I’m packing just necessary things, otherwise travelling can become a big challenge.

Write Your Comment

Please DO NOT include links, URLs or HTML in your comments - they will be automated deleted and you will waste your time.